Public organizations operate under unique financial frameworks that demand specialized accounting practices tailored to their mission-driven objectives. Unlike their private sector counterparts who chase profits, government entities must demonstrate fiscal responsibility, transparency, and accountability to the taxpayers who fund them. This fundamental difference shapes everything they do financially. Government accounting provides the essential infrastructure that enables public organizations to manage resources effectively, comply with regulatory requirements, and maintain the trust of the communities they serve. The specialized field encompasses methodologies, standards, and reporting mechanisms designed specifically to address the complex needs of municipalities, state agencies, federal departments, and other governmental bodies. Through rigorous financial management practices, public organizations optimize resource allocation, ensure compliance, and deliver the essential services their communities depend on daily.

Enhanced Transparency and Accountability

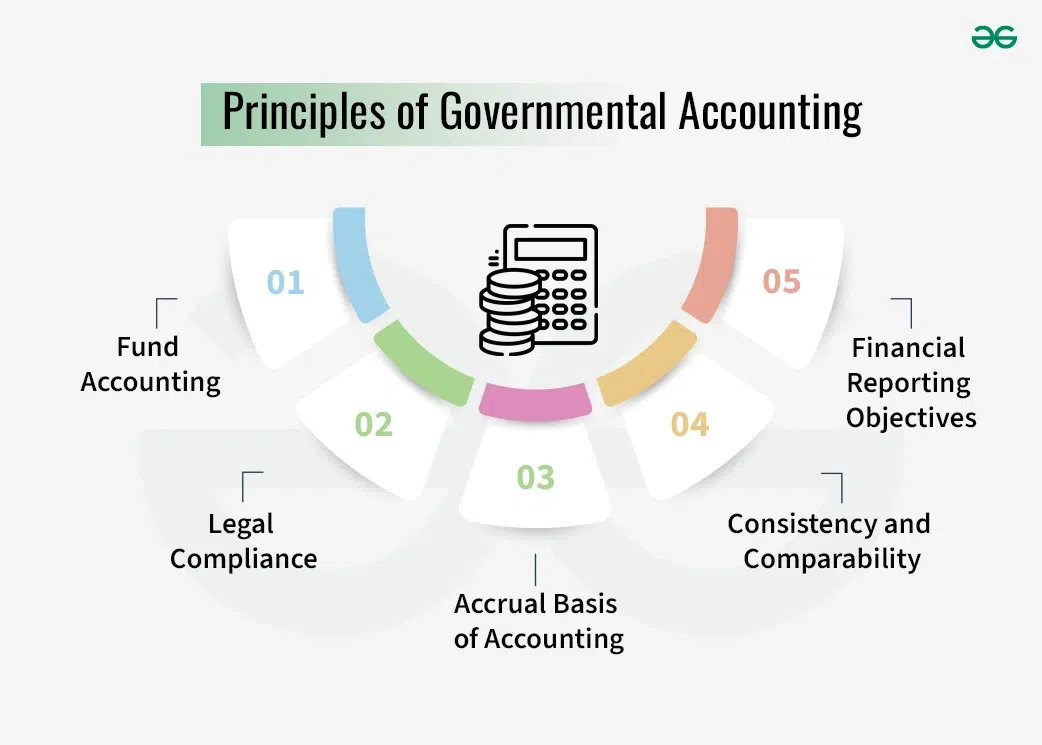

Transparency isn’t just a buzzword in government accounting, it’s the foundation of public trust. Government accounting establishes comprehensive frameworks that promote clear visibility in public financial management, ensuring that every dollar spent can be traced and justified to the people who matter most: the citizens. Public organizations operate under intense scrutiny from citizens, oversight bodies, and regulatory agencies, which makes transparent accounting practices absolutely non-negotiable. Through detailed fund accounting systems, government entities segregate resources according to specific purposes, restrictions, and legal requirements, providing crystal-clear visibility into how funds get utilized across programs and initiatives.

Compliance with Complex Regulatory Requirements

Navigating the regulatory landscape of public finance can feel like solving a puzzle with constantly changing pieces. Public organizations must juggle an intricate web of federal, state, and local regulations that govern financial management and reporting. Government accounting systems are specifically designed to ensure compliance with standards established by the Governmental Accounting Standards Board, which provides authoritative guidance for public sector financial reporting that differs dramatically from private sector requirements. These standards address unique governmental concerns such as fund accounting, modified accrual basis reporting, and government-wide financial statements that you won’t find in traditional business accounting.

Improved Budget Management and Forecasting

When you’re working with taxpayer dollars, every budgeting decision carries weight. Effective budget management represents a cornerstone of responsibility for public organizations charged with delivering services within constrained resources. Government accounting provides the analytical tools and reporting capabilities necessary to monitor budget performance continuously throughout the fiscal year, not just at year-end when it’s too late to adjust. Through sophisticated systems that track appropriations, encumbrances, and actual expenditures, financial managers can identify spending trends and potential budget shortfalls before they become critical.

Support for Grant Management and Funding Compliance

Grants represent critical lifelines for many public programs, but they come up with strings attached that require careful management. Public organizations frequently rely on grants and intergovernmental assistance to fund programs and capital projects, creating complex accounting challenges that can overwhelm standard financial systems. When managing multi-source funding streams, public entities often partner with providers of government accounting services to establish specialized functionality for tracking grant-funded activities separately while integrating them into overall financial reporting. These systems enable organizations to monitor grant expenditures against award budgets, ensuring that spending remains within authorized amounts and eligible cost categories, a requirement that grantors take very seriously. Proper documentation of grant-related costs becomes streamlined through accounting practices that capture detailed transaction information, supporting documentation, and allocation of methodologies automatically. Public organizations must often demonstrate matching fund requirements or cost-sharing arrangements, which government accounting systems track meticulously to prove compliance when auditors come calling. Timely and accurate financial reporting to grantor agencies represents a critical requirement that specialized accounting practices fulfill through automated reporting capabilities that reduce manual effort and errors. By maintaining rigorous controls over grant accounting, public organizations protect their eligibility for future funding opportunities and avoid the serious consequences of grant mismanagement that can include repayment demands and disbarment from future awards. Government accounting also facilitates the reconciliation of grant receivables and manages the cash flow timing differences between when you spend the money and when you get reimbursed, a challenge that can strain operating budgets if not handled properly.

Strengthened Internal Controls and Fraud Prevention

Protecting public resources from misuse isn’t just good practice, it’s a sacred trust that government organizations must honor. Public organizations bear a special responsibility to protect community resources from misuse, waste, and fraudulent activity through robust internal control frameworks that leave no room for carelessness. Government accounting establishes segregation of duties, authorization protocols, and reconciliation procedures that create multiple checkpoints throughout financial processes, making it difficult for errors or intentional misconduct to slip through undetected. These controls reduce opportunities for irregularities while providing detection mechanisms that identify suspicious activities promptly, before small problems become major scandals.

Conclusion

Government accounting serves as the bedrock foundation for effective financial management in public organizations, enabling them to fulfill their missions while maintaining the fiscal responsibility that taxpayers rightfully expect. Through enhanced transparency, regulatory compliance, improved budget management, grant oversight, and strong internal controls, specialized accounting practices address the unique challenges facing governmental entities in ways that traditional business accounting simply can’t match. Public organizations that invest in robust government accounting systems position themselves to deliver superior services, maintain stakeholder confidence, and achieve the long-term financial sustainability that allows them to serve their communities for generations. As public expectations for accountability continue to rise and financial environments become increasingly complex, the critical role of government accounting in supporting public organizations will only expand and evolve.